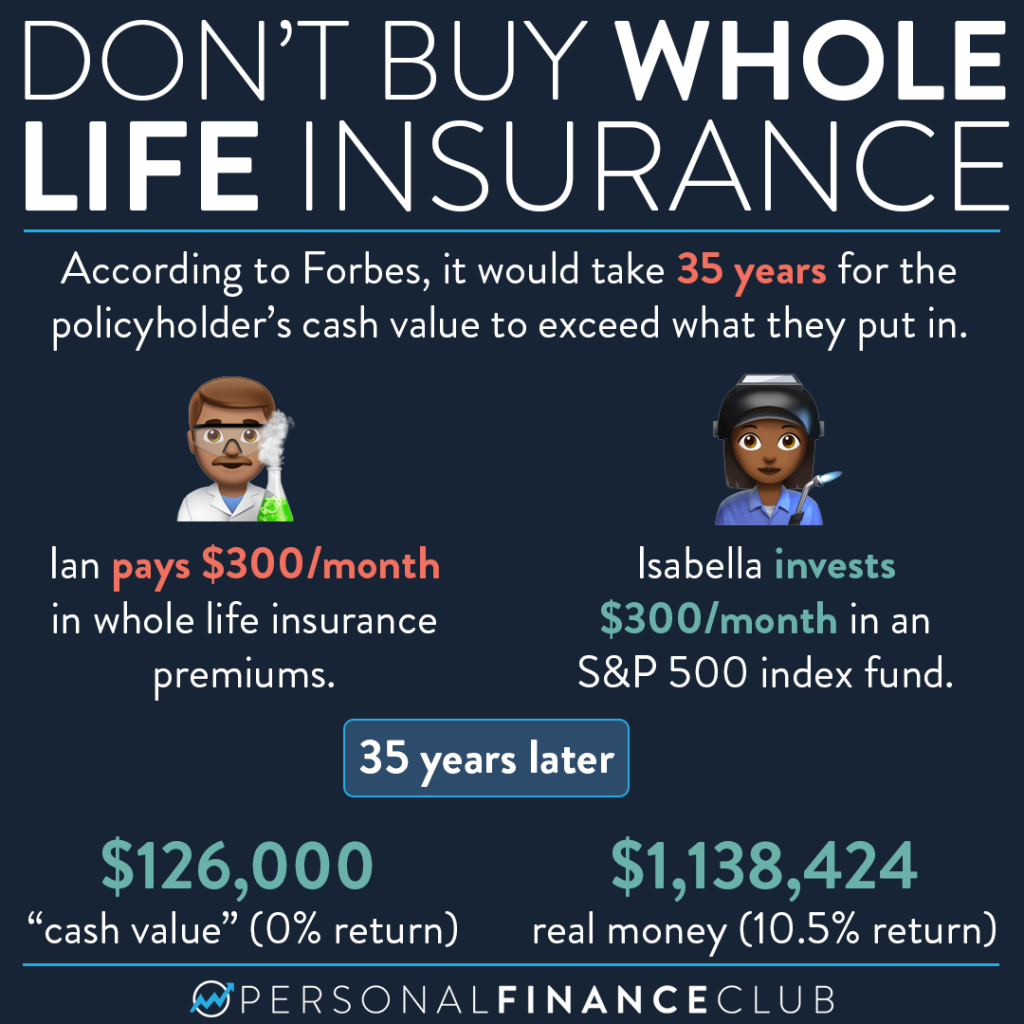

Understanding Whole Life Insurance: Key Benefits and Features

Understanding Whole Life Insurance is essential for anyone looking to secure their financial future. Unlike term insurance, which provides coverage for a specified period, whole life insurance offers lifetime protection and comes with a cash value component that accumulates over time. This dual-layer benefit means that not only does your policy pay out a death benefit to your beneficiaries, but it also serves as a savings tool that can be accessed during your lifetime. The predictable premiums and guaranteed growth make whole life insurance a compelling choice for those seeking stability in their financial planning.

One of the key features of whole life insurance is its tax-deferred growth. As your cash value grows, you won’t have to pay taxes on those gains, which can significantly enhance your savings over the long term. Additionally, policyholders can borrow against the cash value, offering a source of funds for emergencies or investment opportunities. However, it’s essential to understand that any outstanding loans will reduce the death benefit. Overall, recognizing the key benefits and features of whole life insurance can empower individuals to make informed decisions about their life insurance options.

Is Whole Life Insurance Right for You? Pros and Cons Explained

When considering whether whole life insurance is right for you, it’s essential to weigh the pros and cons. On the positive side, whole life insurance provides a guaranteed death benefit, ensuring that your beneficiaries will receive a payout upon your passing. Additionally, it accumulates cash value over time, which can be borrowed against or withdrawn, making it a potentially valuable financial asset. However, one must also consider the higher premiums associated with whole life policies compared to term life insurance. These costs can strain your budget, particularly if you are in the early stages of your financial journey.

On the downside, while whole life insurance offers lifelong coverage, it may not be necessary for everyone. Some individuals may find that term life insurance better suits their needs, especially if they require coverage only for a specific period, such as until children are grown or debts are paid off. Moreover, the investment component of whole life insurance often grows slower than other investment vehicles, which might not be the most efficient use of your money in the long run. Ultimately, your personal financial situation, goals, and preferences should dictate whether whole life insurance is the right fit for you.

How Whole Life Insurance Builds Cash Value Over Time

Whole life insurance is more than just a policy that provides a death benefit; it also accumulates cash value over time. This cash value is a living benefit that grows at a guaranteed rate, allowing policyholders to borrow against it or withdraw funds during their lifetime. The growth of cash value in whole life insurance is typically tax-deferred, meaning you won’t owe taxes on the gains until you withdraw them. This feature makes whole life insurance not only a safety net for your family but also a strategic tool for financial planning.

As policyholders make their regular premium payments, a portion goes towards the cash value, which generally increases steadily. This compounding effect plays a crucial role in building wealth; as the cash value grows, it can also increase the policy’s death benefit. Additionally, whole life insurance policies often participate in dividends, which can further enhance cash value accumulation. Overall, understanding how whole life insurance builds cash value over time can empower individuals to make more informed decisions in their financial journey.